Market Outlook

March 07, 2018

Market Cues

Domestic Indices

Chg (%)

(Pts)

(Cl ose)

Indian markets are likely to open flat tracking global indices and SGX Nifty.

BSE Sensex

(1.3)

(430)

33,317

U.S. stocks showed a lack of direction over the course of the trading session. The

Nifty

(1.1)

(110)

10,249

major averages spent the day bouncing back and forth across the unchanged line.

Mid Cap

(0.8)

(137)

16,168

The Dow Jones rose 0.1% to end at 24,884. The NASDAQ gained 0.6% to close at

Small Cap

(1.3)

(236)

17,652

7,371.

Bankex

(1.4)

(402)

27,551

U.K. stocks extended gains from the previous session as worries about an imminent

trade war eased and Prime Minister Theresa May said she was confident of reaching

Global Indices

Chg (%)

(Pts)

(Cl ose)

a good Brexit deal. The FTSE 100 is up by 0.9% to end at 7,181.

Dow Jones

0.1

10

24,884

On domestic front, Indian shares fell sharply with banking stocks coming under

Nasdaq

0.6

41

7,372

heavy selling pressure once again, after the CBI detained the vice president of

FTSE

0.9

65

7,181

Gitanjali Group and the Serious Fraud Investigation Office (SFIO) summoned ICICI

Nikkei

1.8

376

21,418

Bank chief Chanda Kochhar and Axis Bank's Shikha Sharma in relation to the multi-

crore Punjab National Bank (PNB) fraud case.

Hang Seng

2.1

624

30,511

Shanghai Com

1.0

33

3,290

News Analysis

Government banks wrote off Rs 816.83 billion loans in FY17

A dvances / Declines

BSE

NSE

Detailed analysis on Pg2

Advances

653

404

Declines

2,072

1,415

Investor’s Ready Reckoner

Unchanged

148

55

Key Domestic & Global Indicators

Stock Watch: Latest investment recommendations on 150+ stocks

Volumes (` Cr)

Refer Pg5 onwards

BSE

4,036

Top Picks

NSE

29,813

C MP

Target

U psi de

C ompany

Sector

R ating

(`)

(`)

(%)

Blue Star

Capital Goods Accumulate

793

867

9.4

Net Inflows (` Cr)

Ne t

Mtd

Ytd

Dewan Housi ng Finance

Financials

Buy

508

720

41.6

FII

424

424

916

Century Plyboards

Forest Products

Buy

323

400

23.8

*MFs

1,673

13,261

22,284

Navkar Corporation

Other

Buy

169

265

57.3

KEI Industrie s

Capital Goods

Buy

370

436

17.8

More Top Picks on Pg4

Top Gainers

Price (`)

Chg (%)

Vakrangee

171

5.0

Key Upcoming Events

Previous

C onsensus

Bomdyeing

268

4.3

D ate

Region

Event Description

Reading

Expectations

Bajajelec

567

4.1

Mar07

Euro Zone Euro-Zone GDP s.a. (QoQ)

0.60

0.60

Carboruniv

351

3.8

Mar08

China

Exports YoY%

11.10

11.00

Bpcl

444

2.2

Mar08

US

Initial Jobless claims

210.00

220.00

Mar08

Euro Zone ECB announces interest rates

-

-

Mar09

US

Change in N onfarm payrolls

200.00

205.00

Top Losers

Price (`)

Chg (%)

More Events on Pg7

Beml

1,259

(7.5)

Adanient

186

(7.5)

Balramchin

100

(6.8)

Bankindia

103

(6.5)

Radico

320

(5.9)

As on March 06 2018

Market Outlook

March 07, 2018

News Analysis

Government banks wrote off Rs 816.83 billion loans in FY17

According to reports, Loans worth Rs 816.83 billion were written-off by public

sector banks (PSBs) in 2016-17. In a written reply, Finance Minister Jaitley said that

writing-off of loans is done for tax benefit as well as capital optimisation and

borrowers of such loans continue to be liable for repayment.

As per the Reserve Bank of India (RBI) guidelines and policy approved

by Bank Boards, non-performing loans, including those in respect of which full

provisioning has been made on completion of four years, are removed from the

balance-sheet of the bank concerned by way of write-off.

Economic and Political News

Government banks wrote off Rs 816.83 billion loans in FY17

Auction of 5 mineral blocks in Odisha to take off in April, tender floated

RBI set to give government Rs 100 billion interim dividend

Corporate News

ITC keen to invest in organic farming, aqua cultivation in Odisha

Near-term worries for Maruti stock, even as product demand remains strong

RInfra wins Rs 50bn in DMRC arbitration award, will use funds to pare debt

Infosys unveils technology and innovation hub in Indianapolis for employees

Market Outlook

March 07, 2018

Top Picks

Market Cap

C MP

Target

Upside

C ompany

R ationale

(` Cr)

(`

(`)

(%)

Strong growth in domestic business due to its leade`hip

in acute therapeutic se gment. Alkem expects to launch

Alkem Laboratories

27,056

2,263

2,441

7.9

more products in USA, w hich bode s for its i nternational

busine ss.

Favorable outlook for the AC industry to augur well for

Cooling products busi ness which is out pacing the

Blue Star

7,607

793

867

9.4

market growth. EMPPAC division' s profitability to

improve once operating environment turns around.

With a focus on the low and me dium income (LMI)

consumer segment, the company has increased its

Dewan Housi ng Finance

15,946

508

720

41.6

presence in tier-II & III cities where the growth

opportunity i s immense.

Loan growth is likely to pick up after a sluggish FY17.

Lower credit cost will help in strong bottom-line growth.

Karur Vysya Bank

7,486

103

160

55.3

Increasing share of CASA will help in NIM

improve ment.

High order book execution in EPC segment, rising B2C

KEI Industrie s

2,901

370

436

17.8

sales and higher exports to boost the revenues and

profitability

Expected to benefit from the lower capex requirement

Music Broadcast

2,139

375

475

26.7

and 15 ye ar long radio broadcast licensing.

Massive capacity expansion al ong with rail advantage

Navkar Corporation

2,536

169

265

57.3

at ICD as well CFS augur well for the company

Strong brands and distribution network would boost

Siyaram Silk Mills

3,019

644

851

32.1

growth going ahe ad. Stock currently trades at an

inexpensive valuation.

Market leadership in Hindi news genre and no.

2

viewership ranking in English news genre, exit from the

TV Today Network

2,687

451

508

12.8

radio busine ss, and anticipated growth in ad spends by

corporate to benefit the stock.

After GST, the company is expected to see higher

volume s al ong with i mproving product mix. The Gujarat

Maruti Suzuki

2,60,352

8,619

10,619

23.2

plant will also enable higher operating leverage which

will be margin accretive.

We expect loan book to grow at 24.3% over next two

GIC Housing

2,109

392

655

67.3

year; change in borrowing mix will help in NIM

improve ment

We expect CPIL to re port net Revenue/PAT CAGR of

~17%/ 16% over FY2017-20E mainly due to healthy

7,176

323

400

23.8

growth in plywood & lamination business, forayed into

Century Plyboards India

MDF & Particle boards on back of strong brand &

distribution network.

We expect sales/PAT to grow at 13.5%/20% over next

LT Foods

2,859

89

128

43.2

two years on the back of strong distribution network &

addition of new products in portfolio.

Third large st brand pl ay in luggage segment Incre ase d

product offerings and i mproving di stribution network i s

Safari Industries

1,182

531

650

22.4

leading to strong growth in business. Likely to post

robust growth for next 3-4 years

We expect HSIL to re port PAT CAGR of ~15% over

FY2017-20E owing to better improve ment in operating

HSIL

3,096

428

510

19.1

margin due price hike in container glass segment,

turnaround in consumer business.

We expect financialisati on of savings and increasing

Aditya Birla Capital

35841

158

230

45.5

penetration in Insurance & Mutual fund w ould e nsure

steady growth.

Source: Company, Angel Research

Market Outlook

March 07, 2018

Fundamental Call

Market Cap

C MP

Target

Upside

C ompany

R ationale

(` Cr)

(`)

(`)

(%)

CCL is likely to maintain the strong growth trajectory

CCL Products

3,922

295

360

22.1

over FY18-20 backed by capacity expansi on and new

geographical foray

We forecast Nilkamal to report top-line CAGR of ~9%

to `2,635cr over FY17-20E on the back of healthy

Nilkamal

2,501

1,676

2,178

29.9

demand growth in pl astic division. On the bottom -line

front, we estimate ~10% CAGR to `162cr owing to

improve ment in volumes.

We expect sales/PAT to grow at 9%/ 14% over next two

years on the back of healthy demand growth in

Shreyans Industries

209

152

247

63.0

printing. Further, China had banned maki ng paper

from waste pulp which would benefit Indian paper

companie s.

The prism has diversified exposure in the different

segment such as Cement, Tile & ready mix concrete.

Prism Cement

6,138

122

160

31.2

Thus we believe, PCL is in the right place to capture

ongoing government spendi ng on affordable housing

and infrastructure projects.

Elantas Beck India is the Indian market leader in liquid

insulation segment use d in electrical equipments like

Elantas Beck India Ltd

1,586

2,000

2,500

25.0

motors, transformers etc. It derives demand from

several industries which are expected to register 10%+

CAGR in demand in the coming years.

RPL to report healthy top-line CAGR of ~13% over

FY17-20E on the back of healthy de mand in printing &

Ruchira Papers Ltd.

382

170

244

43.3

writing paper segments. On the bottom-line front, we

estimate ~16% CAGR over FY17-20E owing to strong

improve ment in operating performance.

Greenply Industries Ltd (GIL) manufactures plywood &

allied products and medium density fibreboards

(MDF). GIL to report net reve nue CAGR of ~14% to

Greenply Industries

4,096

334

395

18.3

~`2,478cr over F Y2017-20E mainly due to healthy

growth in plywood & lamination busine ss on the back

of strong brand and di stribution network

Source: Company, Angel Research

Market Outlook

March 07, 2018

Key Upcoming Events

Global economic events release calendar

Bl oomberg Data

D ate

Time

C ountry

Event Description

Unit

Period

L ast Reporte d

E stimate d

Mar 07, 2018

3:30 PM Euro Zone

Euro-Zone GDP s.a. (QoQ)

% Change

4Q F

0.60

0.60

Mar 08, 2018

China

Exports YoY%

% Change

Feb

11.10

11.00

7:00 PM US

Initial Jobless claims

Thousands

Mar 3

210.00

220.00

6:15 PM Euro Zone

ECB announces interest rates

%

Mar 8

-

-

Mar 09, 2018

7:00 PM US

Change in N onfarm payrolls

Thousands

Feb

200.00

205.00

3:00 PM UK

Industrial Production (YoY)

% Change

Jan

-

1.90

7:00 AM China

Consumer Price Index (YoY)

% Change

Feb

1.50

2.50

7:00 PM US

Unnemployment rate

%

Feb

4.10

4.00

Mar 12, 2018

5:30 PM India

Industrial Production YoY

% Change

Jan

7.10

Mar 13, 2018

6:00 PM US

Consumer price index (mom)

% Change

Feb

0.50

0.10

Mar 14, 2018

12: 00 PM India

Monthly Wholesale Prices YoY%

% Change

Feb

2.84

US

Producer Price Index (mom)

% Change

Feb

0.70

Mar 15, 2018

India

Imports YoY%

% Change

Feb

26.10

India

Exports YoY%

% Change

Feb

9.10

Mar 16, 2018

3:30 PM Euro Zone

Euro-Zone CPI (YoY)

%

Feb F

1.20

6:45 PM US

Industrial Production

%

Feb

(0.05)

0.30

6:00 PM US

Building permits

Thousands

Feb

1,377.00

1,310.00

6:00 PM US

Housi ng Starts

Thousands

Feb

1,326.00

1,278.00

Mar 20, 2018

8:30 PM Euro Zone

Euro-Zone Consumer Confidence

Value

Mar A

0.10

3:00 PM UK

CPI (YoY)

% Change

Feb

3.00

Mar 21, 2018

7:30 PM US

Existing home sales

Million

Feb

5.38

3:00 PM UK

Joble ss claims change

% Change

Feb

(7.20)

11: 30 PM US

FOMC rate decision

%

Mar 21

1.50

1.75

Mar 22, 2018

2:00 PM Germany

PMI Manufacturing

Value

Mar P

60.60

Source: Bloomberg, Angel Research

Market Outlook

March 07, 2018

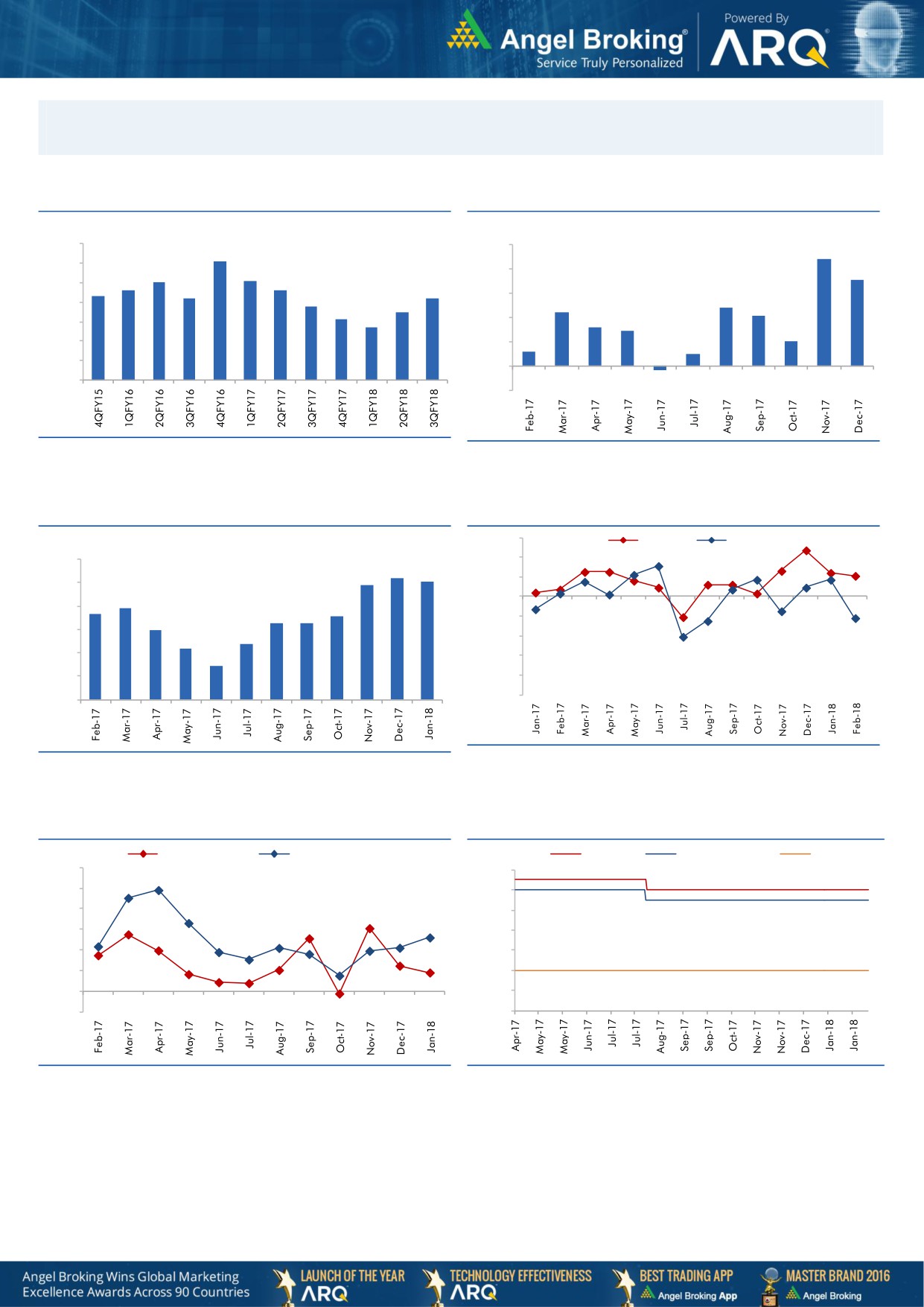

Macro watch

Exhibit 1: Quarterly GDP trends

Exhibit 2: IIP trends

(%)

(%)

10.0

10.0

9.1

8.8

9.0

8.0

8.1

8.0

7.1

7.6

7.6

8.0

7.3

7.2

7.2

6.8

6.0

4.8

7.0

6.5

4.4

6.1

4.1

5.7

4.0

3.2

2.9

6.0

2.0

5.0

2.0

1.2

1.0

4.0

-

3.0

(0.3)

(2.0)

Source: CSO, Angel Research

Source: MOSPI, Angel Research

Exhibit 3: Monthly CPI inflation trends

Exhibit 4: Manufacturing and services PMI

56.0

Mfg. PMI

Services PMI

(%)

6.0

54.0

5.2

5.1

4.9

52.0

5.0

3.9

50.0

3.7

3.6

4.0

3.3

3.3

3.0

48.0

3.0

2.4

2.2

46.0

2.0

1.5

44.0

1.0

42.0

40.0

-

Source: Market, Angel Research; Note: Level above 50 indicates expansion

Source: MOSPI, Angel Research

Exhibit 5: Exports and imports growth trends

Exhibit 6: Key policy rates

(%)

Exports yoy growth

Imports yoy growth

(%)

Repo rate

Reverse Repo rate

CRR

60.0

6.50

50.0

6.00

40.0

5.50

30.0

5.00

20.0

4.50

10.0

4.00

0.0

3.50

(10.0)

3.00

Source: Bloomberg, Angel Research

Source: RBI, Angel Research

Market Outlook

March 07, 2018

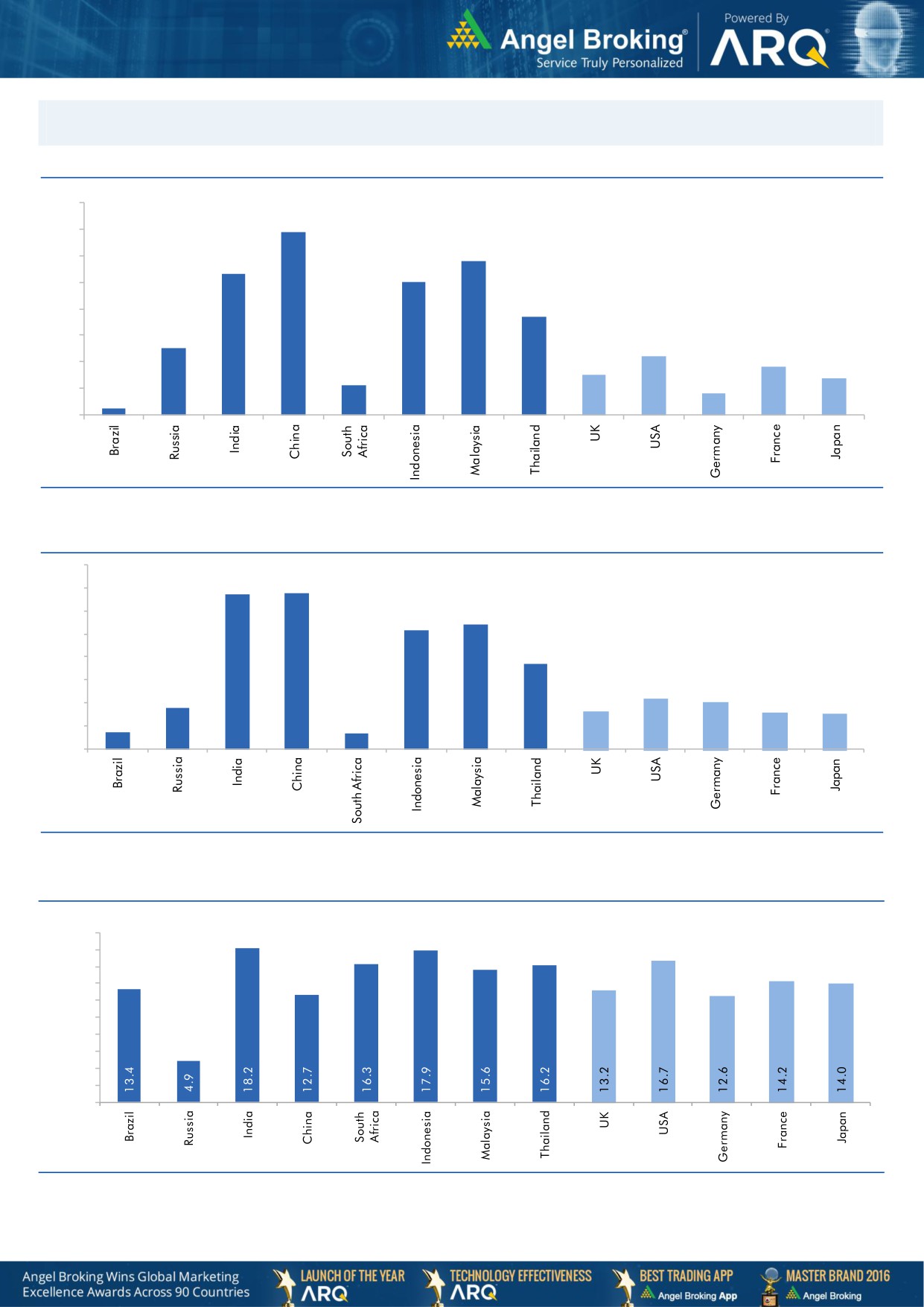

Global watch

Exhibit 1: Latest quarterly GDP Growth (%, yoy) across select developing and developed countries

(%)

8.0

6.9

7.0

5.8

6.0

5.3

5.0

5.0

1.1

3.7

4.0

2.5

3.0

2.2

1.8

2.0

1.5

1.4

0.8

1.0

0.3

-

Source: Bloomberg, Angel Research

Exhibit 2: 2017 GDP Growth projection by IMF (%, yoy) across select developing and developed countries

(%)

6.7

6.8

7.0

6.0

5.4

5.2

5.0

3.7

4.0

3.0

1.8

2.2

2.0

1.7

1.6

2.0

0.7

1.5

0.7

1.0

-

Source: IMF, Angel Research

Exhibit 3: One year forward P-E ratio across select developing and developed countries

(x)

20.0

18.0

16.0

14.0

12.0

10.0

8.0

6.0

4.0

2.0

-

Source: IMF, Angel Research

Market Outlook

March 07, 2018

Exhibit 4: Relative performance of indices across globe

Returns (%)

C ountry

Name of index

Closing price

1M

3M

1YR

Brazil

Bovespa

86,023

1.8

16.2

25.4

Russia

Micex

2,310

0.4

10.1

12.9

India

Nifty

10,359

(7.1)

0.2

14.6

China

Shanghai Composite

3,257

(7.5)

(1.3)

1.1

South Africa

Top 40

51,022

0.4

(1.5)

16.8

Mexico

Mexbol

47,721

(5.4)

0.2

0.6

Indonesia

LQ45

1,090

(2.4)

5.8

20.6

Malaysia

KLCI

1,843

(1.5)

7.1

8.1

Thailand

SET 50

1,190

(0.8)

8.3

20.5

USA

Dow Jones

24,875

(4.9)

3.9

18.7

UK

FTSE

7,116

(5.0)

(2.9)

(3.0)

Japan

Nikkei

21,042

(8.9)

(6.4)

9.1

Germany

DAX

12,091

(4.3)

(4.9)

2.3

France

CAC

5,167

(3.1)

(2.2)

4.2

Source: Bloomberg, Angel Research p68in4

Market Outlook

March 07, 2018

Research Team Tel: 022 - 39357800

DISCLAIMER

Angel Broking Private Limited (hereinafter referred to as “Angel”) is a registered Member of National Stock Exchange of India

Limited,Bombay Stock Exchange Limited and Metropolitan Stock Exchange Limited. It is also registered as a Depository Participant with

CDSL and Portfolio Manager with SEBI. It also has registration with AMFI as a Mutual Fund Distributor. Angel Broking Private Limited is a

registered entity with SEBI for Research Analyst in terms of SEBI (Research Analyst) Regulations, 2014 vide registration number

INH000000164. Angel or its associates has not been debarred/ suspended by SEBI or any other regulatory authority for accessing

/dealing in securities Market. Angel or its associates/analyst has not received any compensation / managed or

co-managed public offering of securities of the company covered by Analyst during the past twelve months.

This document is solely for the personal information of the recipient, and must not be singularly used as the basis of any investment

decision. Nothing in this document should be construed as investment or financial advice. Each recipient of this document should make

such investigations as they deem necessary to arrive at an independent evaluation of an investment in the securities of the companies

referred to in this document (including the merits and risks involved), and should consult their own advisors to determine the merits and

risks of such an investment.

Reports based on technical and derivative analysis center on studying charts of a stock's price movement, outstanding positions and

trading volume, as opposed to focusing on a company's fundamentals and, as such, may not match with a report on a company's

fundamentals. Investors are advised to refer the Fundamental and Technical Research Reports available on our website to evaluate the

contrary view, if any.

The information in this document has been printed on the basis of publicly available information, internal data and other reliable

sources believed to be true, but we do not represent that it is accurate or complete and it should not be relied on as such, as this

document is for general guidance only. Angel Broking Pvt. Limited or any of its affiliates/ group companies shall not be in any way

responsible for any loss or damage that may arise to any person from any inadvertent error in the information contained in this report.

Angel Broking Pvt. Limited has not independently verified all the information contained within this document. Accordingly, we cannot

testify, nor make any representation or warranty, express or implied, to the accuracy, contents or data contained within this document.

While Angel Broking Pvt. Limited endeavors to update on a reasonable basis the information discussed in this material, there may be

regulatory, compliance, or other reasons that prevent us from doing so.

This document is being supplied to you solely for your information, and its contents, information or data may not be reproduced,

redistributed or passed on, directly or indirectly.

Neither Angel Broking Pvt. Limited, nor its directors, employees or affiliates shall be liable for any loss or damage that may arise from

or in connection with the use of this information.